McDonald's Corp is a global leader in the fast-food industry, known for its extensive menu featuring burgers, fries, breakfast items, and beverages. The company operates thousands of restaurants worldwide, serving millions of customers daily. McDonald's focuses on consistent quality, convenience, and affordability, while also adapting its offerings to cater to local tastes and dietary preferences. In addition to its iconic drive-thru service, the company has embraced technology by implementing digital ordering platforms and mobile apps, enhancing customer experience. Through its commitment to innovation and sustainability, McDonald's continues to shape the fast-food landscape while promoting responsible sourcing and reducing its environmental impact. Read More

While strong cash flow is a key indicator of stability, it doesn’t always translate to superior returns. Some cash-heavy businesses struggle with inefficient...

McDonald's (NYSE:MCD) has outperformed the market over the past 20 years by 1.85% on an annualized basis producing an average annual return of 11.08%. Currently, McDonald's has a market capitalization of $199.83

Even if a company is profitable, it doesn’t always mean it’s a great investment. Some struggle to maintain growth, face looming threats, or fail to reinvest ...

What Happened? Shares of fast-food chain McDonald’s (NYSE:MCD) jumped 3.6% in the afternoon session after a report from UBS highlighted the company as an att...

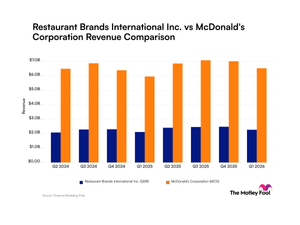

Restaurant Brands International posted Q1 2026 revenue of $2.26 billion and EPS of 86 cents, as Burger King U.S. comparable sales surged 5.8% amid its ongoing turnaround.

McDonald's (NYSE:MCD) has outperformed the market over the past 20 years by 1.86% on an annualized basis producing an average annual return of 11.02%. Currently, McDonald's has a market capitalization of $194.15